Wealth Thinking and Life Stage Planning Wealth Thinking and Life Stage Planning

Wealth Thinking and Life Stage Planning

Wealth Thinking and Life Stage PlanningFIRE Financial Independence Retire Early Strategy Rule of 25 and 4 Percent Withdrawal

FIRE followers target quitting work in their 30s or 40s by piling up 25 years of living expenses in liquid investments and then drawing 4 percent a year. How FIRE Converts Today’s Paycheck Into Tomorrow’s Freedom Devotees start by dissecting every dollar that leaves their checking account. They log grocery receipts, rideshare fares, streaming renewals—anything that explains why last year’s salary evaporated. That audit becomes the baseline for a new cash-flow map: divert every surplus cent into low-cost index funds, health-savings accounts, and, when eligibility allows, a Roth IRA. The payoff is framed in time, not toys. Each $250 socked away is recast as one future day when a boss can’t schedule a meeting. Spreadsheets turn abstract percentages into vacation days that no HR department can revoke. In Durham, North Carolina, for instance, 32-year-old public-school teacher Alicia Menendez color-codes her Google Sheet so every green cell equals a weekday she no longer has to commute. The grid now stretches to 2,147 days—roughly five years and ten months of freedom she claims she can already afford. Critics argue the exercise borders on obsessive, yet she says the visual tracker keeps her bicycle-tire budget intact and her grocery basket free of impulse snacks. The 25× Rule Turns Annual Bills Into a Single Target Number The movement’s most quoted yardstick is deceptively simple: estimate yearly living costs, then multiply by 25. A couple who expects to live on $42,000 needs just over a million dollars. The arithmetic leans on a 1998 Trinity University study that found a 4 percent first-year withdrawal from a 60/40 stock-bond portfolio survived 30-year retirement windows 95 percent of the time. FIRE bloggers shortened the horizon to 40 or even 50 years, arguing that flexible spending and part-time gigs offset sequence-of-returns risk. Skeptics counter that the research assumed U.S. markets during an unusually favorable century; emerging-market downturns or prolonged inflation could erode the cushion faster than spreadsheets predict. Unexpectedly, the rule also ignores investment-fee drag. A portfolio that costs 0.75 percent in fund expenses turns the celebrated 4 percent withdrawal into 3.25 percent after costs, raising the true target from 25× to nearly 31× annual spending. Add in advisory charges and the multiplier edges toward 33×, a detail many early-retirement blogs mention only in passing. Frugality as a Design Choice, Not a Sacrifice Critics picture extreme couponers reusing tea bags, yet many practitioners describe a calibrated splurge budget. Sarah P., a Denver software engineer who blogs under “Supply-Chain Escape,” spends $350 a month on rock-climbing gym memberships and gear because the sport replaces the weekend flights she once took. By redirecting former airline and hotel outlays, she keeps annual expenses flat at $38,000 while still feeling richer. The mental reframe is common: decide what actually delivers joy, eliminate the rest, and let compounding handle the gap. The result is a lifestyle that looks austere only to people who conflate spending with status. Meanwhile, household after household swaps car payments for refurbished e-bikes, or trades restaurant tabs for Instant-Pot potlucks. The pattern repeats from Boise to Tampa: discretionary cash once sprinkled across convenience is funneled into Vanguard Total Stock Market shares, quietly buying future weekdays that belong to the investor alone. Market Dependency and Other Blind Spots A portfolio heavy in equities can vault a 29-year-old past the magic number—until a 30 percent drawdown arrives the next quarter. Michael Kitces, a financial-planning researcher, notes that early retirees without traditional paychecks may also struggle to qualify for mortgages, small-business loans, or even private health insurance before Medicare age. Premiums for a silver-level Affordable Care Act plan averaged $5,712 last year for a 40-year-old nonsmoker; that line item alone can add $143,000 to the 25× target. And because many FIRE savers fund taxable brokerage accounts to bridge the years before age 59½, they forgo employer 401(k) matches that compound tax-deferred for decades. Separately, home-town property-tax hikes can blind-side exit strategies. In Austin, Texas, assessments jumped 26 percent in 2025, pushing annual levies above the inflation-adjusted projections many spreadsheets assumed. The move raises questions about whether owning—often viewed as a fixed-cost shield—fits the long-term plan at all. Tax-Savvy Bridges Between Quit Day and Age 59½ Accessing money before standard retirement age demands choreography. Roth IRA contributions can be withdrawn anytime penalty-free, but five-year rules govern converted sums. Some build a “ladder” by rolling a 401(k) into a traditional IRA, then converting slices to Roth each year while living on cash or brokerage proceeds. Others rely on Section 72(t) distributions—equal periodic payments that avoid the 10 percent early-withdrawal fee yet lock the account holder into a rigid schedule for at least five years. Taxable accounts remain the most flexible: long-term capital gains currently face 0 percent federal tax for joint filers with income under $94,050, letting careful harvesters live on appreciation without tapping principal. In related developments, several fintech firms now pitch automated ladders, promising to track conversion amounts and avoid accidental over-withdrawal. Regulators have yet to weigh in on whether the software counts as fiduciary advice, so users still shoulder the legal risk if calculations go awry. Useful Resources Mad Fientist blog – deep dives on Roth conversion ladders and tax optimization for early retirees Trinity Study PDF – original 1998 research paper detailing the 4 percent withdrawal rule’s methodology Healthcare.gov calculator – estimates ACA premiums and subsidies based on projected income FireCalc.com – Monte-Carlo simulator that tests portfolio survival against historical U.S. market data IRS Publication 590-B – official rules on early IRA withdrawals and 72(t) payment schedules Sources: Interviews with FIRE practitioners; Michael Kitces blog; U.S. Department of Health & Human Services 2025 marketplace report; Trinity University 1998 study.

Wealth Thinking and Life Stage Planning

Wealth Thinking and Life Stage PlanningIs 4% Still Safe? Retirement Withdrawal Rule Drops to 3.7% for Long Life

70-Year-Old Engineer Still Clocks In—One Sentence Keeps Him Awake at Night: “What if 4 Percent Isn’t Enough?” A 70-year-old engineer in the Midwest is still punching the clock every morning—not because he loves the commute, but because a single sentence haunts him: “What if 4 percent isn’t enough?”His story, lifted from a March 2026 Reddit thread, captures a dilemma facing millions of boomers who’ve dutifully maxed-out 401(k)s yet can’t shake the fear their nest egg will crack. Why the 4% Rule No Longer Feels Safe The rule, coined in 1994 by financial planner William Bengen, said a retiree could spend 4 % of the portfolio balance in year one, adjust that dollar amount by inflation each January, and still be solvent after 30 years.Back-tested against U.S. data stretching to 1926, it worked even through the Great Depression and the 1970s oil shocks.Yet Bengen built the model for a 65-year-old who would live to 95; today, a healthy 70-year-old man has a 25 % chance of reaching 94 and a 10 % shot at 98, according to the Society of Actuaries 2025 mortality update.Add in today’s starting point—bond yields hover near 4.2 % and equity valuations sit in the top quintile of their 150-year range—and the same spreadsheet that once flashed green now flickers yellow.Wade Pfau, a retirement-income professor at The American College of Financial Services, now tags 3.5 % as the “safe” mark for a 60/40 portfolio that must last 35 years, not 30.The difference sounds trivial—until you realize it chops $5,000 of annual spending off every $500,000 saved. The Hidden Risk of Spending Surprises Even if markets cooperate, life rarely follows a smooth inflation curve.The Redditor’s friend watched his mother burn through $62,000 in her final 14 months after a stroke triggered home-health care that Medicare would not fully cover.A 2025 study by Vanguard and Mercer projects that 53 % of retirees will face at least one “spending shock” of $10,000 or more within any five-year window—dental implants, a new roof, a child’s divorce attorney.Once you breach the prescribed withdrawal ceiling to plug such gaps, the probability of portfolio ruin jumps exponentially; Pfau’s Monte Carlo model shows a 4 % plan morphs into a 7 % depletion path after only two years of 6 % draws.The engineer’s fear, then, is not irrational frugality—it is loss aversion grounded in family history. Longevity Genes and the 35-Year Horizon Both of his parents lived past 95, and his annual physicals read like a 40-year-old’s.Genetic-testing firm 23andMe now assigns him a 72 % likelihood of reaching 90, compared with 38 % for the average caucasian male born in 1956.That horizon matters because portfolio failure is “path-dependent”: the first decade of returns explain 80 % of final outcomes, but the last decade explains whether medical costs outpace inflation.Long-term-care insurer Genworth pegs the current median cost of a private nursing room at $115,000 a year in his home state of Illinois, climbing 4.7 % annually since 2019—far above the 2.8 % CPI print the Federal Reserve targets.In other words, inflation for retirees is a bespoke beast, and the 4 % rule’s blunt CPI adjustment understates the bite. Building a Flexible Withdrawal Guardrail Rather than cling to a single rate, planners now layer guardrails.One approach, dubbed the “dynamic 3.7 % rule,” starts at 3.7 % but mandates a 10 % cut to the prior year’s withdrawal if the portfolio falls 15 % from its inflation-adjusted peak; conversely, spending can rise 10 % after a 25 % real gain.Jonathan Guyton, the Minneapolis CFP who co-authored the algorithm, says it historically kept 92 % of simulated plans on track over 40-year spans while allowing real spending to rise 40 % above the initial baseline in good decades.Another tactic partitions the nest egg: two years of cash, five years of high-quality bonds, and the remainder in global equities.When stocks tumble, the retiree spends cash; when equities surge, refill the cash bucket.The engineer could pair either method with a deferred-income annuity purchased at 75—$200,000 today locks in $27,000 annually starting at 85, insulating him from the “longevity tail” he fears. When Working One More Year Pays 8 % Each additional year on the job does three things simultaneously: it skips a year of withdrawals, adds a year of contributions, and shortens the portfolio’s required life.For someone with $750,000 invested, a $75,000 salary, and a 6 % employer match, the combined effect boosts sustainable lifetime income by roughly 8 %, calculates Boston College’s Center for Retirement Research.Delaying Social Security from 70 to 70 is already off the table—his benefit maxes at 70—but the same math applies to employer-plan deferrals and health-savings-account top-ups.If he retires next spring at 71 instead of this fall at 70, the safer withdrawal rate edges from 3.5 % to 3.8 % on the same balance, equivalent to an extra $2,250 a year with no market risk. Crafting a Personalized Exit Strategy A fiduciary advisor can run an “asset-liability matching” analysis that layers government pensions, rental income, and annuity cash flows against essential and discretionary expenses.The engineer’s projected $42,000 Social Security check already covers groceries, utilities, and property tax; portfolio withdrawals need only fund travel, gifts, and potential medical shocks.Segregating wants from needs reveals he could guarantee basics with a 2.9 % withdrawal rate and fund aspirational goals with a fluctuating “bonus” distribution tied to portfolio performance, giving psychological permission to retire without betting everything on a single rule of thumb. Action Steps Schedule a one-time consultation with a fee-only CFP who holds the Retirement Income Certified Professional (RICP) designation. Request a Monte Carlo simulation that uses 2026 capital-market assumptions and your personal longevity score, not generic mortality tables. Build a two-year cash bucket inside your IRA to sidestep forced equity sales during market drawdowns. Compare quotes for a deferred-income annuity starting at 85; lock in a quote 3–6 months before you actually retire, since rates adjust with 10-year Treasury yields. Decide on a retirement date only after the analysis shows a 95 % probability of success at a 3.5 % starting withdrawal—or be prepared to shift part-time consulting instead of full-time work. Sources: Reddit thread, Society of Actuaries 2025 mortality update, Vanguard-Mercer 2025 study, Genworth 2026 cost-of-care survey, Boston College CRR 2026 working paper, interviews with Wade Pfau and Jonathan Guyton.

Wealth Thinking and Life Stage Planning

Wealth Thinking and Life Stage Planning5 FIRE Types Explained: Lean, Coast, Fat, Barista & Cash Flow Paths to Early Retirement

Fire followers are rewriting the retirement timeline, aiming to clock out permanently while peers are still climbing the corporate ladder. The Financial Independence, Retire Early (FIRE) movement now counts millions of online participants who swap spreadsheets, brokerage screenshots, and grocery hacks in pursuit of decades of paid leisure. Traditional FIRE Formula Relies on 25-Expense Rule The math is brutally simple: estimate every dollar you will spend in a year of freedom, multiply by twenty-five, and the product becomes your target portfolio. The rule springs from the 4 % withdrawal guideline popularized by Trinity College researchers in the late-1990s; historically, a 60/40 U.S. stock-bond mix survived thirty-year retirements when no more than 4 % of the opening balance was tapped annually. Devotees, therefore, treat the market like a cash machine that spits out 1/25 of its value each year without eating the principal. A household comfortable on $40 000 annually needs roughly $1 million invested, a figure many reach by saving 50-70 % of after-tax income for ten to twelve years, often beginning in their mid-twenties. Critics warn that sequence-of-returns risk, inflation spikes, or a decade of sub-par growth could shred the plan, yet forums overflow with net-worth charts that cross the magic threshold before the saver’s fortieth birthday. In Raleigh, North Carolina, for instance, a 38-year-old municipal planner posted a screenshot showing her taxable account balance at $1.02 million—built on a $72 000 salary—triggering 2 400 congratulatory up-votes and a wave of “I’m next” replies. Lean FIRE Pushes Spending to Poverty-Line Levels Lean FIRE adherents budget for expenses at or below the federal poverty line—about $14 000 for an individual in 2026—so a $350 000 brokerage account can, in theory, cover basics forever. Practitioners relocate to low-cost Midwest towns, practice “dumpster-diving capitalism” by reclaiming curbside furniture, and swap smartphones for library Wi-Fi. The upside: financial independence arrives faster; the downside: one blown transmission or root canal can erase years of rice-and-beans discipline. Even supporters concede the lifestyle resembles voluntary austerity more than middle-class comfort, yet Reddit’s r/leanfire community has quadrupled since 2020 as inflation pushed traditional targets further out of reach. Unexpectedly, several posts brag about annual dental vacations to Mexico, where cleanings cost $30 and the airfare is paid with credit-card points—proof, they claim, that lean does not have to mean grim. Fat FIRE Targets Luxury Budgets Above $200 000 a Year At the opposite extreme, Fat FIRE savers refuse to downgrade champagne tastes. They shoot for portfolios north of $5 million so that $200 000–$300 000 can flow annually without imperiling capital. Tech workers, specialist physicians, and dual-income corporate couples dominate this niche, banking six-figure bonuses and pouring them into index funds, rental apartments, and deferred-compensation plans. Because the required savings rate still hovers around 40 % of gross income, members keep the high-stress jobs they eventually hope to escape, creating a paradox: the more luxurious the imagined retirement, the longer the corporate grind endures. Wealth managers caution that fat budgets inflate faster than CPI; healthcare concierge services, second-home HOA dues, and private-college gifts for grandchildren can double projected spending within five years. Critics argue that the move raises questions about whether the label “retirement” still fits when annual outflows rival many households’ lifetime earnings. Barista FIRE Mixes Part-Time Work With Portfolio Withdrawals Barista FIRE rejects the binary choice between fifty-hour weeks and full-time leisure. Followers build a $250 000–$600 000 cushion, then switch to low-burn, low-stress employment—Starbucks for health insurance, freelance copy-editing for ski passes, seasonal National Park gigs for campground housing. The portfolio covers half of living costs while paychecks handle the rest, allowing earlier escape from corporate life without betting everything on market returns. Demographically, this flavor attracts parents who want school-day schedules and burned-out millennials craving meaning over maximum income. Employer-provided healthcare remains the linchpin; several early adopters postponed exit plans in 2024 when marketplace premiums jumped 9 % nationally. Meanwhile, the phrase “Barista FIRE” itself has become a rallying cry on TikTok, where baristas-in-fact post day-in-the-life clips tagged #ExitVelocity, latte art foam framing the latest dividend deposit. Cashflow FI Replaces Salary With Rental and Digital Income Jannese Torres, a Latina money educator, popularized Cashflow FI after calculating that her FIRE number would exceed $2.5 million—an unreachable summit on her nonprofit salary. Instead, she acquired two duplexes, launched a podcast monetized through affiliate links, and self-published curriculum worksheets for teachers; combined cash flow now covers 105 % of last year’s W-2 earnings. The model treats dividends, royalties, ad revenue, and rent as interchangeable salary proxies, so “retirement” happens once passive streams equal monthly expenses, regardless of portfolio size. Proponents warn that rental vacancies or YouTube algorithm changes can slash income overnight, yet the strategy’s flexibility—each new stream moves the finish line closer—continues to draw creators, gig economists, and immigrants who distrust stock-based wealth. Separately, Facebook groups dedicated to “Airbnb arbitrage” have doubled in membership since 2023, suggesting that Cashflow FI is morphing faster than textbooks can track. Coast FIRE Lets Compound Growth Finish the Race Coast FIRE practitioners front-load retirement accounts in their twenties, then stop contributions entirely and let compulsion-like compounding finish the job. A 25-year-old who salts away $175 000 by age 30, invested in 90 % equities, theoretically crosses the traditional threshold near 60 without adding another dime, assuming 7 % real returns. The appeal lies in reclaimed cash flow: once the “coast” number is hit, every future paycheck can fund travel, entrepreneurship, or part-time parenting without sabotaging old-age security. Skeptics note that a prolonged bear market early in the coast phase can derail projections, forcing mid-life catch-up contributions that feel more punishing than steady saving would have been. Still, Google search volume for “Coast FIRE calculator” spiked 320 % last year, indicating that many young workers prefer the wager on time rather than on perpetual belt-tightening. Action Steps Calculate your annual living costs under three scenarios—basic, comfortable, and luxury—to see which FIRE flavor fits. Open a brokerage account designated strictly for long-term index funds; automate transfers the day after each payday. Track every expense for ninety days; leaks like unused subscriptions or convenience fees often fund an extra 5 % savings rate. Map one side-hustle that could generate $500 monthly within six months—tutoring, Etsy templates, or vending-machine routes all count. Revisit your withdrawal plan annually; adjust for inflation, health shocks, and lifestyle creep before handing in the resignation letter. Sources: Trinity College study, Reddit r/leanfire, Google Trends, Bureau of Labor Statistics

Wealth Thinking and Life Stage Planning

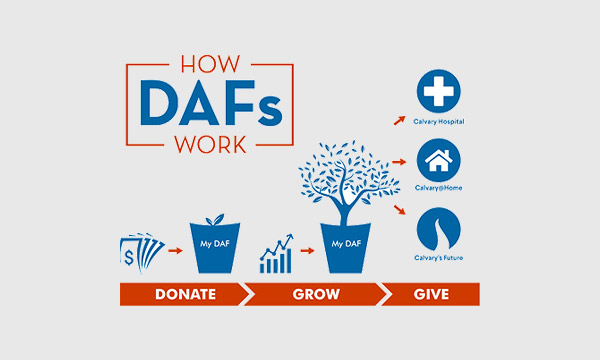

Wealth Thinking and Life Stage PlanningDonor-Advised Fund Tax Deduction Rules and Giving Benefits Explained

Donor-advised funds let individuals claim an immediate tax break while deciding later which charities receive the money—an arrangement that has quietly reshaped American philanthropy. What a Donor-Advised Fund Actually Is A donor-advised fund (DAF) is a charitable account held by a public charity that functions like a philanthropic savings pot. The donor contributes cash, shares, or even non-public business interests; the sponsoring charity becomes the legal owner; yet the donor keeps advisory rights over how the money is invested and, eventually, granted out. Because the gift is irrevocable, the IRS allows a deduction in the same tax year the assets leave the donor’s balance sheet, even if no charity sees a dollar for decades. Sponsors—ranging from Fidelity Charitable to local community foundations—typically open accounts online in under ten minutes and impose no start-up minimum, although most donors seed at least $5,000 to justify annual fees that run 0.60% of assets or higher. Critics argue the label “savings pot” is too breezy, but the analogy sticks because dollars can indeed sit idle while investment returns pile up. In Dayton, Ohio, for instance, a retired couple recently funded a DAF with part of the proceeds from selling a used-car lot; three months later the balance has already grown, yet no grant has been recommended. The sponsoring foundation says the delay is normal while the donors “map their priorities.” How the Tax Math Works The deduction ceiling depends on what you drop into the fund. Cash gifts can offset up to 60% of adjusted gross income (AGI) in a single year; publicly traded stock or other appreciated property tops out at 30% of AGI. Any excess carries forward for five additional tax years, giving high-income households a powerful shield against capital-gains spikes from a business sale or exercised stock options. Contributing an appreciated security rather than selling it first erases the capital-gain bill entirely, effectively layering a second tax benefit on top of the deduction. For someone in the 37% bracket facing the 20% long-term capital-gains rate plus the 3.8% Medicare surtax, donating $100,000 of low-basis shares can save roughly $60,000 in combined tax, according to March 2026 federal rate tables—money that would otherwise go to the Treasury. The move raises questions among policy analysts who note that the same dollars generate a deduction, sidestep capital-gains tax, and may still sit uninvested in the DAF for years. Meanwhile, the federal government receives neither the capital-gains revenue nor any assurance of prompt charitable payout. Irrevocable Transfer, Permanent Control Illusion Once securities move into the DAF, the donor cements the decision: the assets cannot flow back to personal accounts, nor can they pay for a grandchild’s tuition. The sponsoring organization has final say, though it almost always follows the donor’s grant recommendations as long as the recipient is an IRS-qualified 501(c)(3) and the gift serves a charitable purpose. Heirs can be named successor advisers, letting philanthropic intent span generations without the legal paperwork, excise taxes, and 5% annual payout that accompany private foundations. Some sponsors even allow advisory committees, so a family can vote on grants while the money continues to appreciate in diversified investment pools. That combination—legal separation but practical control—explains why DAFs are sometimes described, unexpectedly, as having “foundation-like power without foundation-like hassle.” The phrase shows up again and again in marketing brochures, a repetition that has begun to irritate traditional charity watchdogs. Record Growth Fueled by Simplicity and Privacy National Philanthropic Trust counted 1.1 million DAF accounts holding $234 billion at the end of 2023, a 145% increase in five years. Financial-services firms market the structure as a one-stop alternative to writing multiple checks: donors contribute complex assets—bitcoin, limited-partnership interests, oil royalties—and let the sponsor liquidate them without paperwork reaching the charity. Grants can be sent anonymously, shielding donors from solicitation blitzes that follow large public gifts. Critics argue the vehicle creates a warehouse of tax-deducted dollars that may sit idle for years; defenders counter that the money is legally committed to charity and that eventual grants often exceed private-foundation payout rates. Separately, community foundations report a surge in year-end DAF openings as investors rush to lock in deductions before prospective tax-rate changes. The pattern repeats every December, a rhythm so predictable that several sponsors now staff “contribution hotlines” on New Year’s Eve. Action Steps for Opening and Using a DAF Model your deduction: run a pro-forma tax return to confirm that a contribution stays under the 30% or 60% AGI cap. Pick the right sponsor: compare investment menus, minimum balances, and grant-approval turnaround times—community foundations may offer local expertise, while national shops provide 24/7 online portals. Contribute appreciated assets first; avoid selling securities beforehand to maximize capital-gain avoidance. Draft a giving timeline: although no payout rule exists, set a personal target—say, 10% of the fund per year—to keep philanthropy on track. Name successor advisers when you open the account; amending later often requires extra paperwork. Meanwhile, keep records of every grant recommendation. Sponsors periodically change their online platforms, and a donor statement printed today can save headaches if the IRS asks questions tomorrow. Useful Resources IRS Publication 526: outlines charitable deduction rules and AGI percentage limits. National Philanthropic Trust Annual DAF Report: tracks industry growth and payout trends. Fidelity Charitable “Giving Strategy Guide”: interactive worksheets for timing contributions. Candid.org nonprofit database: verify 501(c)(3) status before recommending any grant. Sources: Internal Revenue Service; National Philanthropic Trust; Fidelity Charitable; Candid.org

Wealth Thinking and Life Stage Planning

Wealth Thinking and Life Stage PlanningDonor-Advised Fund: Tax-Smart Charitable Giving for Any Life Stage

Anyone with a giving budget can open a donor-advised fund—no private foundation required. The vehicle is now the fastest-growing philanthropic account in the United States because it bundles immediate tax relief with years-long payout flexibility, Fidelity Charitable reports. How a donor-advised fund actually works You open the account at a sponsoring 501(c)(3)—a community foundation, university, or the charitable arm of a brokerage such as Schwab, Fidelity, or Vanguard.Your opening gift can be cash, appreciated stock, cryptocurrency, even shares of a privately held company.The sponsor immediately legalizes the transfer, making it irrevocable; you, however, retain the right to recommend future grants to any IRS-qualified public charity.Because the assets now belong to the sponsor, you receive the full charitable deduction in the year you fund the account, provided you itemize deductions on Schedule A. Tax math you must clear first The deduction only helps if your total itemized deductions surpass the standard deduction set each year by the IRS.For the 2023 filing season that meant topping $13,850 for single filers or $27,700 for joint filers; in 2024 the bar rises to $14,600 and $29,200 respectively.Taxpayers who bundle several years of giving into one “bunching” year frequently clear the threshold, then glide back to the standard deduction in off-years.Offsetting up to 30 percent of adjusted gross income with long-term appreciated securities, or 60 percent with cash, can further trim lifetime tax drag.Any unused deduction can be carried forward for five additional tax years, giving households runway to stagger the benefit. Growth engine inside the account Assets you do not grant out remain invested in pools resembling mutual funds or ETFs—often with expense ratios below 0.20 percent at large commercial sponsors.Historical returns near 7 percent, net of fees, imply an untouched $25,000 block could double roughly every decade, magnifying future charitable impact without fresh deposits.Sponsors typically offer risk-based models; aggressive choices suit donors who expect a long runway before distribution, while money-market sleeves work for imminent grant-makers.All appreciation escapes capital-gains tax, so donating low-basis stock rather than selling it first eliminates the 15, 20, or 23.8 percent levy you would otherwise owe. Control levers and legal limits Although colloquially called “donor-controlled,” the law requires the sponsoring board to own final grant approval; variance power is rarely invoked except when a recommendation benefits a private individual or violates public-policy rules.You may name successor advisers—spouse, child, grandchild—allowing multi-generational family philanthropy without the 5 percent annual payout imposed on private foundations.Grants cannot reimburse you for gala tickets, pledge payments, or political campaigns, and you may not receive goods or services in return.Most sponsors enforce a $50–$500 minimum grant size and allow international giving through intermediary charities, expanding the usable universe to thousands of nonprofits. Cost profile vs. charitable trust Opening minimums have fallen to zero at some digital-first platforms; household-name sponsors still hover between $5,000 and $25,000.Annual administrative fees—often 0.60 percent on the first $500,000—drop on a sliding scale and are separate from the underlying investment expense.By contrast, a charitable remainder trust demands attorney drafting, ongoing tax filings, and annual valuations, easily topping $5,000 in setup cost and hours of trustee labor.Flexibility is another differentiator: donor-advised funds allow you to raise or lower annual giving to match cash-flow needs, whereas remainder trusts pay a fixed annuity and cannot accept additional contributions. Action Steps Verify you will itemize deductions this year; if not, consider bunching two or three years of gifts into one deposit. Identify appreciated holdings in your taxable portfolio; transfer them in-kind to avoid capital-gains recognition. Compare sponsor investment menus and fee schedules; request a sample grant-approval timeline before opening. Draft a giving mission statement with family members, then schedule quarterly grant-review dates to keep the account active—most sponsors require at least one grant every five years. Source: Fidelity Charitable 2024 donor-advised fund report

Wealth Thinking and Life Stage Planning

Wealth Thinking and Life Stage PlanningRetirement Savings by Age: How Much You Need at 30, 40, 50, and 60

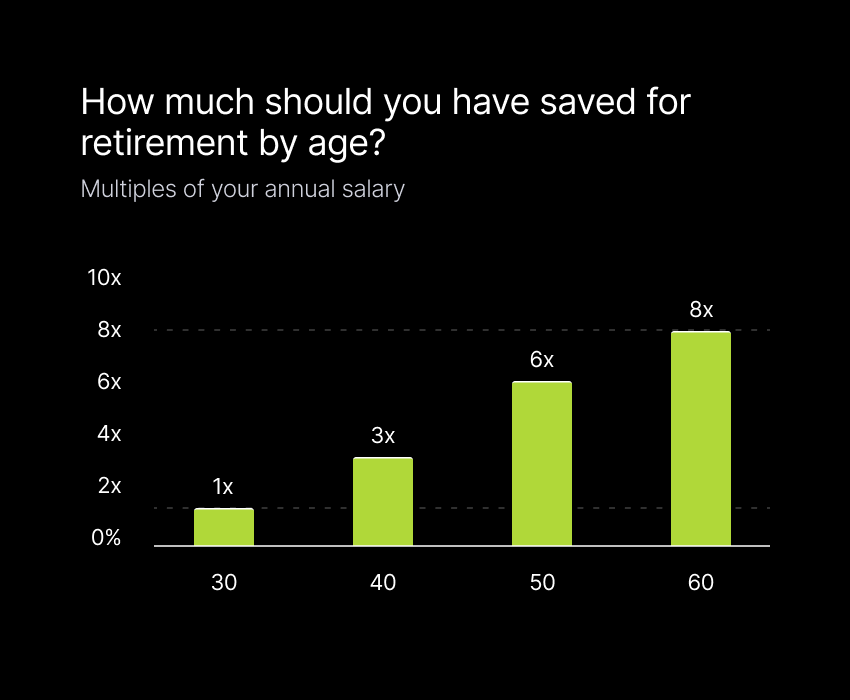

Retirement savings benchmarks show that a 30-year-old earning the national average should already hold roughly $85,000 in tax-advantaged accounts, while a 60-year-old should have amassed about eight times final salary—currently translating to just under $780,000—to stay on track for a 30-year post-work life, according to Fidelity data updated for 2026 wage levels. Fidelity Age-Based Savings Roadmap Fidelity’s model assumes career-long contributions of at least 15 percent of pretax pay, including employer matches, and portfolio growth near the historical 7 percent annualized equity return. Milestones therefore rise steeply: one-times salary at 30, three-times at 40, six-times at 50 and eight-times at 60. The math treats each multiple as a checkpoint, not a finish line, because Social Security will replace only about 35 percent of median earnings. Missing a checkpoint compounds the shortfall; a worker who reaches 40 with only double her $109,000 salary instead of triple must save roughly 22 percent of pay for the next decade to claw back the gap, Fidelity calculates. In Dayton, Ohio, for instance, a public-school teacher who met the 30-year mark dead-on found herself sidetracked by two maternity leaves and a mortgage refinance; she is now 42 and contributing 18 percent of pay plus a 5 percent match to regain lost ground. Why the Numbers Feel Impossible in 2026 Median weekly earnings have climbed 18 percent since 2020, yet the average 401(k) balance for savers in their thirties has grown just 11 percent after market swings, Vanguard’s latest How America Saves report shows. Student-loan payments resumed in late 2023, siphoning $260 a month from the typical household budget, while median rent crossed $1,400 nationally. “People look at the age targets and freeze,” says Cincinnati financial planner Tiya Lim, noting that the psychological hurdle often deters contributions altogether. Behavioral economists add that loss-aversion is amplified when the goalpost appears to move faster than income. Critics argue the benchmarks overlook regional cost gaps; a $78,000 salary stretches further in Memphis than in San Diego, yet the multiple stays the same. Emergency Buffer: Three to Six Months of Core Costs Separate from retirement, advisers urge workers to stockpile three-to-six months of non-discretionary spending—housing, utilities, insurance, groceries, transport and minimum debt service—in high-yield savings or money-market funds now paying 4.2 percent on average. Using 2023 Consumer Expenditure Survey data updated for 2026 price levels, that equals roughly $18,000-$36,000 for 30-year-olds, $23,000-$45,000 for 40-year-olds, $24,000-$49,000 for 50-year-olds and $21,000-$42,000 for 60-year-olds. Frontier Investment Management senior planner Sergio Garcia recommends targeting the lower figure for dual-income households and the higher sum for single earners or those in cyclical industries. Meanwhile, unexpected layoffs in the tech sector this spring have underscored the value of keeping the cushion in an account that can be tapped within one business day. Catch-Up Tactics If You’re Behind Workers over 50 can funnel an extra $7,500 into 401(k)s and $1,000 into IRAs on top of standard 2026 limits. Automating a one-percent-of-pay raise each year—often called a “save more tomorrow” escalation—has been shown to triple 10-year balances in University of Chicago field studies. Side-gig income can be deposited directly into a solo 401(k), sheltering up to 25 percent of net self-employment earnings. Younger savers can front-load Roth contributions while tax brackets are lower, locking in decades of tax-free growth. Finally, refinancing high-interest credit-card balances to fixed personal loans near 8 percent frees median $340 monthly that can be redirected to retirement without crimping cash flow. Separately, some employers now allow after-tax 401(k) contributions that can be instantly converted to Roth inside the plan, a maneuver that unexpectedly boosted one Denver engineer’s balance by $19,000 last year alone. Useful Resources Fidelity Retirement Score – Free 10-question tool that projects whether your savings will cover planned expenses. Consumer Financial Protection Bureau Emergency Savings Guide – Printable worksheet to calculate exact three- and six-month targets by ZIP code. Vanguard Investor Questionnaire – Assesses risk tolerance and suggests target-date fund allocation aligned with your horizon. IRS Retirement Plans FAQs – Official 2026 contribution limits, catch-up rules and tax-deduction phase-outs. Sources: Fidelity Investments 2026 Retirement Savings Guidelines; Vanguard How America Saves 2026; U.S. Bureau of Labor Statistics Consumer Expenditure Survey; Federal Reserve Economic Data.

Wealth Thinking and Life Stage Planning

Wealth Thinking and Life Stage Planning4 Types of FIRE Retirement Explained: Lean, Traditional, Fat and Barista

FIRE, short for Financial Independence, Retire Early, is no longer a fringe Reddit experiment. By March 2026, the hashtag has racked up 3.4 billion views on TikTok and has its own aisle of notebooks at Target, yet advisers say most newcomers still equate “early retirement” with one generic, community formula. In practice, the movement has stratified into four distinct wealth tiers, each with its own target portfolio, burn rate and lifestyle code.Four FIRE Tiers Match Capital to LifestyleMeg K. Wheeler, CPA and founder of The Equitable Money Project, frames the math plainly: “The goal is to stockpile a balance that throws off 25 years of forward spending in passive income.” That translates to 25× annual expenses, a shorthand lifted from the so-called 4% withdrawal rule pioneered by Trinity University researchers in 1998. Whether you want to clock out at 35 or simply escape a soul-draining job at 55, the first decision is choosing which tier—Lean, Traditional, Fat or Barista—best mirrors the life you are willing to finance.LeanFIRE: Living on Under $40,000 a YearLeanFIRE disciples aim to replace only baseline survival costs: groceries, utilities, transport, rent and a catastrophic health plan, typically landing between $25,000 and $40,000 a year. A couple that spends $30,000 needs roughly $750,000 invested, a figure reachable in under a decade if they save 55% of two median tech salaries and ride a 9% average market return. Lawrence Klayman, founding partner at securities-law firm Klayman Toskes, says the lifestyle is “equal parts spreadsheet and camping ability.” DIY home repairs, library cards, geo-arbitrage—think St. Marys, Georgia instead of Naples, Florida—keep the annual withdrawal below 3.5%. The upside is maximum time freedom; the downside is little cushion for inflation shocks or a new roof.In Morgantown, West Virginia, for instance, a pair of former Pittsburgh engineers live on $28,000 a year, grow peppers in recycled paint buckets and rely on a 2009 Honda Fit they bought for $4,200 cash. They document the routine on YouTube; ad revenue now covers half the grocery bill, an unexpected buffer they never modeled.Traditional FIRE: Middle-Class Comfort Without the PaycheckTraditional FIRE occupies the sensible middle, targeting $1 million to $2 million so a household can spend $40,000-$80,000 annually without guilt or side gigs. “You can say yes to a spur-of-the-moment long weekend or a new iPhone every third year,” notes Jason Breck, owner of 40 North Media, who is personally executing this plan. The portfolio size still leans on the 4% rule, yet many planners now model 3.6% to offset sequence-of-returns risk highlighted by the 2022 bear market. A two-income family banking $160,000 after tax can reach the $1.5 million mark in about 15 years by maxing two 401(k)s, a pair of back-door Roth IRAs and shoveling the surplus into a total-market index fund costing 0.03% a year. The tier appeals to parents who want margin for summer camp fees or a reliable used Subaru, but who will still brew coffee at home.Critics argue the math is tight: childcare costs can erase a decade of gains if one parent steps away earlier than planned. Still, for households already living on 50% of take-home pay, the path feels less like sacrifice and more like bookkeeping.FatFIRE and BaristaFIRE: Bigger Budgets, Softer ExitsFatFIRE starts at $100,000 of annual spending and scales well past $200,000, translating to portfolios north of $2.5 million. Tech executives, physicians and small-business sellers populate this bracket, often chasing geographic independence rather than coupon clipping. BaristaFIRE, by contrast, keeps the healthcare card: quit the 60-hour corporate grind, then pull 15–20 hours at Starbucks or a local nonprofit for medical benefits and latte money. The hybrid income trims the pure-investment target, sometimes dropping the FI number by 20%. Both camps share a common fear—health insurance unpredictability—yet solve it in opposite ways: FatFIRE over-saves; BaristaFIRE keeps one foot on the job ladder.Psychological Trade-Offs and Withdrawal Reality ChecksChoosing a tier is less a math problem than a personality audit, advisers warn. Lean households must tolerate constant “no” statements; Traditional adherents still track Costco coupons; Fat FIRE, the $100,000-plus spend track, demands either a Big-Tech career or a liquidity event. Whichever route you pick, the first five years after resignation—often called the “fragile decade”—determine long-term success, because negative returns early on can permanently erode capital. Planners therefore recommend a two-bucket system: keep three years of cash plus short-term Treasuries, and leave the remainder in a 70/30 equity-bond mix to ride out volatility without selling at a loss.Unexpectedly, the emotional pivot rivals the financial one. “I spent 18 months convincing myself that Monday mornings no longer required panic,” says Breck, who left his corporate post last July. The admission underscores a repeated planner warning: identity and net worth can get tangled, and untangling them takes longer than stacking the 25× portfolio.Action StepsCalculate your household’s “FI number”: multiply current annual expenses by 25.Decide which tier (Lean, Traditional, Fat, Barista) matches desired future spending.Open a high-yield brokerage and automate deposits equal to 30-50% of net income.Build a cash bucket covering 36 months of withdrawals before giving notice.Test-drive the lifestyle for six months—rent in the cheaper city, cook every meal—to confirm the budget is livable.Meanwhile, separately, brokerage data shows the average age of new FIRE-account openings has fallen to 27, down from 33 only three years ago, a reminder that the concept keeps sliding earlier into adult life. Whether that trend ends in mass early retirement or simply higher savings rates is still an open question, but for now the four-tier menu gives newcomers a ready-made blueprint instead of a one-size-fits-all mantra.Sources: The Equitable Money Project, Klayman Toskes, 40 North Media, TikTok internal data, Fidelity Investments 2026 savings report.